The 2026 Retail Apocalypse Is Creating a Golden Age for Service Franchises

While Macy's shutters 150 stores, GameStop closes 470 locations, and Pizza Hut pulls the plug on 250 restaurants, a different story is unfolding on the other side of the franchise industry. Essential-service franchises, the brands that fix pipes, replace hydraulic hoses, restore flood-damaged buildings, and maintain commercial kitchens, are posting record growth numbers.

According to Coresight Research, an estimated 7,900 U.S. stores will close in 2026. Francesca's is liquidating all 400 locations. Eddie Bauer is shutting every one of its 175 stores. Foot Locker is on track to close 400 locations by year's end.

Yet at the same time, PIRTEK USA, a B2B hydraulic hose service franchise, just posted its strongest year in company history, opening 41 new locations and awarding 61 franchise units in 2025. BELFOR Franchise Group expanded its national footprint across every major brand in its 15-franchise portfolio. And the IFA projects over 12,000 new franchise establishments in 2026, led by service-driven categories.

For franchise investors, the message is clear: the retail closures of 2025-2026 aren't just a crisis, they're a sorting mechanism. And the winners are franchises built around services people and businesses genuinely need, regardless of consumer confidence or economic cycles.

The Numbers Behind the Retail Closure Wave

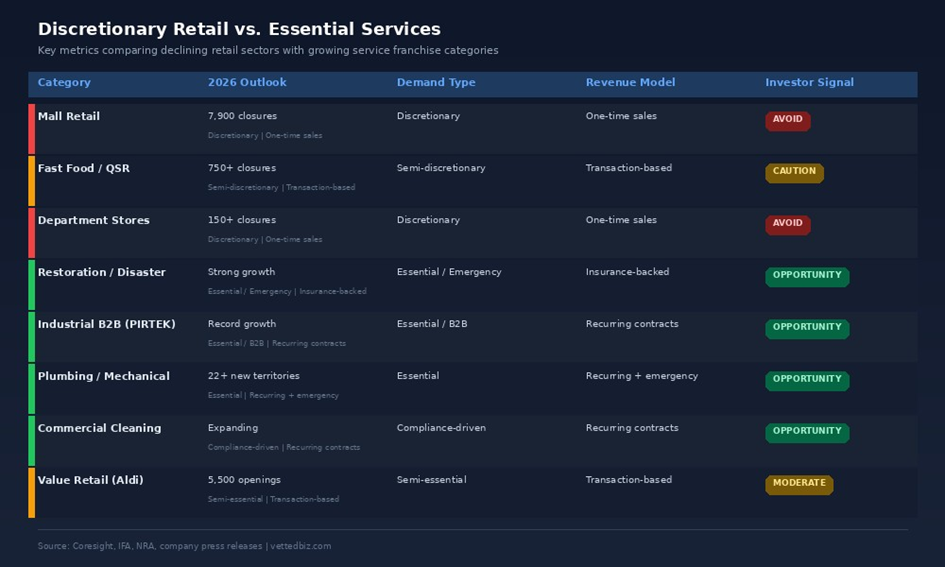

Coresight Research projects approximately 7,900 U.S. store closures in 2026, a 4.5% decline from 2025's even higher figure, but still historically elevated. Among the most significant closures announced for 2026: Francesca's (all 400 locations, full liquidation), Eddie Bauer (all 175 U.S. and Canada stores, bankruptcy), GameStop (470+ stores), Foot Locker (400 stores exiting lower-tier malls), Macy's (150 total locations), Pizza Hut (250 underperforming restaurants), Wendy's (up to 300 locations), and Papa John's (approximately 200 franchise-owned restaurants).

The drivers are familiar but intensifying. E-commerce dominance continues to erode foot traffic. Operating costs, rent, labor, utilities keep rising. Consumer spending patterns have permanently shifted toward convenience and digital-first experiences. And tariff-driven cost pressures are squeezing already-thin margins, with 42% of restaurant operators reporting they were not profitable in 2025.

Key Insight: The closures aren't random. They're concentrated in discretionary retail and consumer-facing categories where demand is elastic. The franchise categories that are growing are the ones where demand is inelastic, where the service must happen regardless of economic conditions.

Why Essential-Service Franchises Are Thriving

Essential-service franchises operate fundamentally differently from discretionary retail in three critical ways.

Demand is tied to necessity, not consumer sentiment. When a hydraulic hose fails on a construction site, a pipe bursts in a commercial building, or flood damage destroys a business, the work must be done immediately. These services aren't discretionary purchases that consumers can defer during a downturn, their emergency responses and maintenance obligations tied to safety, compliance, and operational continuity.

Revenue models are often B2B and recurring. Many essential-service franchises operate in business-to-business environments, serving construction, manufacturing, transportation, healthcare, utilities, and facility management. Commercial contracts, maintenance agreements, and emergency response relationships create predictable, recurring revenue that doesn't depend on foot traffic or impulse buying.

Infrastructure needs grow regardless of economic cycles. The United States has aging infrastructure across commercial buildings, residential properties, industrial facilities, and municipal systems. These systems require ongoing maintenance, repair, and replacement. Economic downturns may defer some maintenance, but they can't eliminate it, and deferred maintenance often creates larger, more expensive service calls later.

The Franchise Categories Leading the Shift

Property Restoration and Disaster Response

Water damage, fire damage, mold remediation, and storm restoration are among the most recession-resistant franchise categories. When disaster strikes, property owners have no choice but to respond, and insurance typically covers the cost, meaning the customer's ability to pay is less affected by economic conditions. BELFOR Franchise Group operates multiple brands in this space, including 1-800 WATER DAMAGE and 1-800-BOARDUP. The group celebrated strong momentum heading into 2026, with expansion across its portfolio of 15 franchise brands spanning restoration, cleaning, plumbing, and commercial services.

Industrial and Commercial Services

PIRTEK USA represents the gold standard for B2B essential-service franchising. The brand provides hydraulic and industrial hose maintenance and replacement, a service that keeps construction equipment, manufacturing lines, and commercial vehicles operational. In 2025, PIRTEK opened a record 41 new locations, awarded 61 franchise units, and expanded to 35 states plus Puerto Rico. The brand's model includes both mobile service units (one-hour on-site ETA, 24/7/365) and retail service centers, serving construction, manufacturing, logistics, transportation, waste management, and utilities.

Plumbing and Mechanical Services

Z PLUMBERZ, part of BELFOR Franchise Group, expanded into 22 new territories in 2025 by combining traditional plumbing expertise with advanced pipe-lining technology. Plumbing emergencies don't wait for economic recoveries, and regulatory requirements around water safety and building codes continue to drive demand.

Commercial Cleaning and Kitchen Exhaust

HOODZ specializes in commercial kitchen exhaust cleaning, a service required by fire code for every restaurant, hotel, hospital, and institutional kitchen. The brand added 12 new units in 2025. Commercial cleaning franchises benefit from regulatory compliance requirements that make the service non-optional.

Service vs. Retail: What the Data Shows

The IFA's 2026 Economic Outlook projects the fastest growth in franchise establishment counts within commercial and residential services and child services, each growing at approximately 3.2%, more than double the overall franchise establishment growth rate of 1.5%.

Meanwhile, Coresight expects about 7,900 retail closures against roughly 5,500 openings, a net loss of approximately 2,400 retail locations. The openings are concentrated among value retailers (Dollar General, Aldi, Tractor Supply) and experiential concepts, while closures hit traditional mall-based retail, department stores, and struggling restaurant chains.

How to Evaluate an Essential-Service Franchise

- Verify the 'essential' claim. Ask: would this service still be purchased during a deep recession? Is demand driven by necessity, regulation, or compliance, or by consumer preference? Brands that rely on discretionary home improvement may label themselves 'services' but face demand elasticity similar to retail.

- Evaluate the revenue model. The strongest essential-service franchises have multiple revenue streams: emergency response (high-margin), maintenance contracts (predictable, recurring), and project-based work. Look for brands where at least 40-50% of revenue comes from recurring or contract-based sources.

- Analyze B2B vs. B2C mix. Franchises with a strong B2B component tend to have more predictable revenue and lower customer acquisition costs. Commercial clients often sign multi-year service agreements, creating a base of recurring income that residential-only models typically can't match.

- Ask about competitive moats. Essential-service franchises that require specialized equipment, certifications, or licensing create natural barriers to entry. Brands with proprietary equipment, insurance industry relationships, or regulatory certifications have competitive advantages that are difficult for new entrants to replicate.

- Review Item 19 and Item 20 carefully. In the FDD, Item 19 will tell you what franchisees are actually earning. Item 20 will reveal system health, openings, closures, and transfers. A service franchise with low closure rates and strong new-unit growth is a positive signal.

- Talk to franchisees about recession performance. Ask current operators how their business performed during the 2020 pandemic shutdowns and any subsequent economic softness. Essential-service franchises that maintained or grew revenue during those periods have demonstrated real recession resistance, not just marketing claims.

The Real Estate Angle: How Retail Closures Create Opportunity

There's a secondary benefit to the retail closure wave that savvy franchise investors should consider: commercial real estate availability. Shopping centers that lost a GameStop or a specialty retailer are actively recruiting service-oriented tenants, fitness studios, medical spas, tutoring centers, and service franchise locations.

For service franchises that benefit from a retail-style storefront (pet grooming, urgent care, auto services), the current environment offers more favorable lease terms, better location options, and reduced buildout costs. And shopping center operators increasingly prefer experiential and service-based tenants who drive regular foot traffic rather than traditional product retailers competing with e-commerce.

The Bottom Line

The 2026 retail closure wave is not a reason to avoid franchise investment, it's a reason to invest more carefully. The 7,900 store closures projected this year are concentrated in discretionary retail and consumer-facing categories where demand is elastic and competition from e-commerce is relentless.

The franchise categories thriving in this environment are the opposite: essential services tied to infrastructure maintenance, emergency response, regulatory compliance, and B2B commercial relationships. These models offer recurring revenue, inelastic demand, and competitive moats that discretionary retail simply can't match.

For franchise investors in 2026, the question isn't whether to invest. It's whether to follow the crowds into the next trendy consumer concept, or to invest in the brands that keep America's buildings, equipment, and infrastructure running regardless of what happens in the economy. The data strongly favors the latter.

Ready to explore your franchise options? Start by requesting FDDs from multiple brands, comparing the real-world cost data from current franchisees, and modeling your investment under realistic cost assumptions. For detailed franchise data, risk scores, and tools to support your due diligence, explore www.vettedbiz.com.

Get insider access to franchise insights

Subscribe to receive expert tips, franchise rankings, and exclusive data straight to your inbox, trusted by thousands of aspiring business owners and investors.

Franchise resources & insights

Explore expert guides, data-driven articles, and tools to help you make smarter franchise decisions, whether you're just starting out or ready to invest.